CASH DOCTOR - “8 Word Healthcare Solution”

Discount for Health, Eliminate out-of-network Penalty & Share Savings

Our Goal

Empowered Consumer + Transparent Free Market = Affordable Healthcare

Robert Stehlin MBA, Cash Doctor, Inc.

After years of research, Cash Doctor has developed a three step plan to transform health care as we know it today.

The goal of the plan is to create a free marketplace controlled by an empowered consumer.

We accomplish this by engaging the consumer in all three stages of healthcare; No Care, Minimal care and Maximum Care.

Save healthcare by transfering the power of choice and the power of the purse into the hands of the consumer.... Healthcare is in the midst of a turbulent global transformation. The need for the reduction in demand is extream. Global health care consumption is approximately 6-7 trillion dollars and is projected to expand to 12 Trillion in the next 6 years, yet there will only be 6-7 trillion dollars to pay for the required services. (Russell Reynolds).

The US healthcare industry is currently undergoing the most significant change since the formation of medicare in the 1960’s. The Affordable Care Act has affected every aspect of the industry from providers to insurance companies all the way to the consumer. All said and done, healthcare costs continue to increase and our current system has not been able to provide a sustainable solution to reverse the trend of even slow it growth. In this model, we have designed three simple steps to repair our 3+ trillion dollar healthcare system.

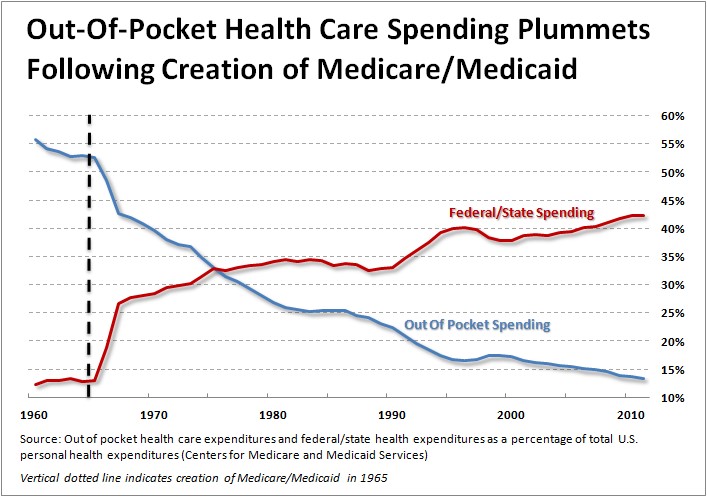

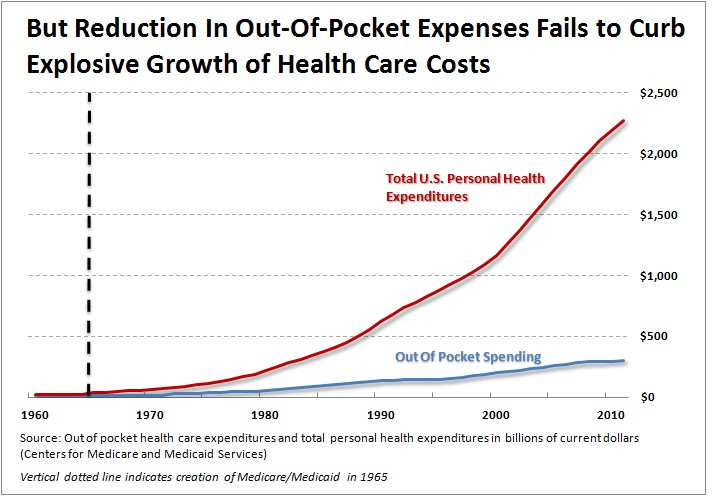

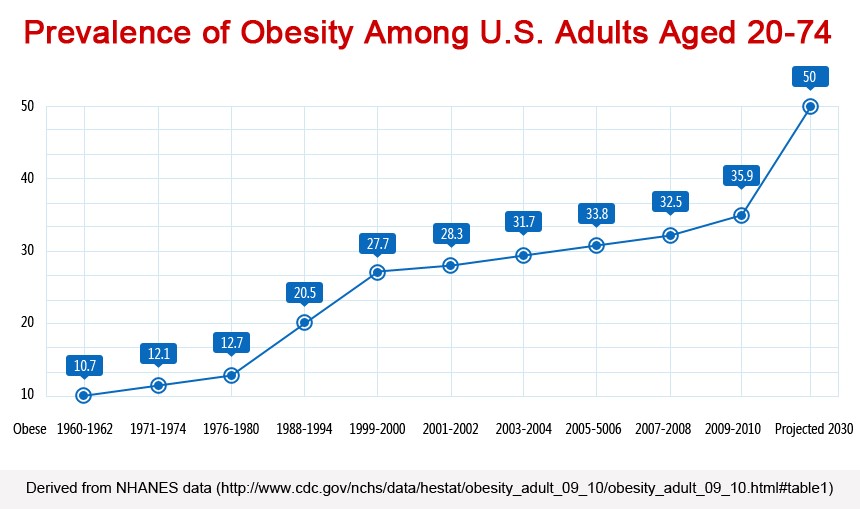

WHAT HAPPENED? - In 1960 the average American paid 55% of the total healthcare bill cash out of pocket and healthcare was just 5% of Gross Domestic Product. Along came the invention of health insurance, managed care, medicare, medicaid and what is now called a “third payer” system creating a whole new layer of cost and disruption. Simply stated, the American citizen consumes medical services, the provider provides the medical services and the third party picks up the tab and sends the bill to the consuming consumer by way of taxes, payroll deductions or diverted compensation. The consumer has no idea as to the cost of the service and has delegated all responsibility to the third party. In 2013 the average American paid only 11% of the total health care bill cash out of pocket and healthcare is now a whopping 20% of our GDP - a 400% increase since the creation of the healthcare industry as we know it today. During this same time where care was to be managed by these newly created intities, obesity rose from a megar 13% to a whopping 33+%. The idea that if you give the consumer a huge list of services, they wil take the right action is just not true.

HOW DID IT HAPPEN? - According to the CDC in 2003, 80 - 90% of all healthcare cost are due to poor lifestyle choices. It appears that consumers have developed a lifestyle of bad choices during a period where the cost of medical services were unknown and paid by a third party. Today, an out of control health care system may be the result of this separation. To accomplish a successful change, we must move the focus of “sick care” away from the providers, employers, government and third party payers and return it to the true payer and consumer of healthcare - the American consumer. By placing the consumer in the controlling role, we will increase innovation and improve our outcomes. Ever since the nation departed from direct consumer payments, cost have spiraled out of control. The solution to our current healthcare crisis and the development of a sustainable model is to return to a payer/consumer centric system of healthcare.

How will it CHANGE! - Change will come when the consumer is empowered and engaged in the all aspects of healthcare and medical services from the beginning to the end, from financing to consumption. The “Best Price Best Value Model” does this in THREE SIMPLE steps. The model is comprised of; lifestyle based risk sharing, price sharing™, and cost participation all working to bring about a TRUE disruption in healthcare. The effects of this combination has been seen in several sub health care markets where technology has improved outcomes and free markets have reduced cost: cosmetic surgery, corrective eye surgery, and dental implants. The rate of change and net benefit to the health consumer works much like interest where it will compound on an annual basis producing gains beyond what we can currently calculate.

By encouraging the American consumer and corporations to support a model of price sharing™, we can start the transition from a third party controlled system (Insurance companies and governments) to one that is controlled directly by the empowered CONSUMER. The “Best Price Best Value model” has three action steps that need to be embraced, adopted and magnified by consumers, our elected officials and our corporate leaders. The first step represents the benefit “before engagement”, the second step represents the benefit of “majority engagement” (80% of the population) and third step represents the benefit of “maximum engagement” (20% of the population). THREE SIMPLE steps, require no financial investment from any of the stakeholders and can revolutionize how the United States cures the healthcare crisis.

DISCOUNT FOR HEALTH - The need to use financial instruments and organizations (medical sharing organizations, self-funded organizations, Health insurance companies and managed care organizations) to share the risk of medical cost among large populations can not be avoided. Risk based pricing needs to be integrated in the insurance priciming model in order to activate and continually motivate a healthy or low risk lifestyle. Risk based pricing can be accomplished by scaling the price of coverage based on risk; lifestyle habits and biometrics of the consumer. By incentivizing healthy low risk lifestyle choices, through reduced premiums, consumers directly benefit from their actions and the actions of their family. UnitedHealth Care is in the process of pilitoing a program that would use a fitness app to track health lifestly habits and reward the consumer for such use by way of rewards and discounts in their local community. Consumer directed financial incentives has a direct effect on their habits. Just being accountable to a concerned party has dramatic results. A recent study tracking activity levels in youth showed a 60% increase when their movements were tracked by their pediatrician. Change can happen, but will only happen when the consumer is empowered with choice and rewarded financially.

ELIMINATE "OUT-OF-NETWORK" Penalty - PwC Research Institute reports in their Top Health Industry Issues for 2015 that 82% of those surveyed said price was most important when making a healthcare purchasing decision while 62% reported high quality ratings by other consumers as the second most popular factor in healthcare purchases. A recent report by AARP in their November 2014 Magazine promoting the benefits of International Medical Tourism failed to identify the power of price transparency in the USA compared to other nations. Out of the 14 catagories reviewed in the report 5 are considered transparent in the USA. Transparent meaning consumers pay for the service because they are elective surgeries not traditionally covered by insurance; breast reduction, breast implant, dental inplats, tummy tucks and gastric bypass. In analyzing the data, Non-transparent procedures were 45% to 65% more expesive than the world averages while the transparent catagories were any where from 35% more expense for tummy tuckes to dental implants being 8% cheaper than the world average. Lastly when a transparent US cash hospital was compared to the world averages in non-transparent medical services; heart bypass was 67% cheaper, masectomy 48% cheaper, spinal fusion 15% cheaper and knee replacement 19% more expensive. On average the US Cash Hospital was a better value than the foreign competition. In conclusion, Americans do not need to go foreign to get value, they just need a transparent marketplace driven by the power of direct cash payments.

No system should provide first dollar coverage in order to maintain constant engagement of the consumer. We do not have first dollar coverage on our car and we should not have it on our body. By requiring consumers to self purchase first dollar services they will benefit directly from the “Best Price” model and the marketplace will be flooded with price conscious shoppers looking for price and value in every local community across the country and the globe. The marketplace will be created to support each particular local community based on free market principles of supply and demand. The sharing of this data via the internet and mobile applications within the general population will create the ever elusive community marketplace Americans have been desiring for the past decade. In order to establish a marketplace where every consumer insured or uninsured to acquire services, the empowered consumer will need insurance contracts that support the direct purchasing from medical providers by applying out of network purchases obtained at or below negotiated network reimbursement as if they are “in network” and are applied 100% against deductible.

SHARE SAVING - Third, and most powerful component of the “Best Price Best Value” model is COST PARTICIPATION. Consumers financially participating in the purchasing of medical services beyond the maximum out of pocket is unheard of. This dynamic change will result in a constant downward pressure being applied to the cost side of the healthcare model and marketplace. Insurance companies can create an incentive program or regulations can be passed requiring or allowing for such programs, based on the “best price model” allowing the consumer to benefit directly from the savings obtained by choosing the lower cost option thus activating an army of 200 million consumers all asking an easy question - HOW MUCH does it cost? The amount of money currently being paid out in claims is huge and the consumer is footing the bill. The amount of savings possible is large, but the consumer must benefit financially if we are going to reach a rate of change great enough to totally disrupt the structure of healthcare. An real life example: Consumer injures knee and required surgery. The current network price in their local area is $8,300 plus $2,100 for MRI. Same consumer can have the same or better service done at another local “cash only” hospital for $3,750 plus $500 for the MRI. The consumer has a $5000 deductible. The consumer can save $1250.00 if he chooses to pay cash. The insurance carrier looks to spend $5400 above the insured deductible. If the carrier applied “cost participation” they would save $6.150 on the operation and split the difference ($3,075) with the consumer by means of prepayed deductibles and future premiums. The net cost to the consumer would be $1,925 instead of the $5,000 they paid, a 58% savings, and while the net cost to the insurnace company is $3,075 instead of the $6,150, a 50% savings, they would have paid under the normal in network reimbursements. It is a win - win - win for the consumer, the insurance carrier and the cash hospital. Only when there is this freedom of choicel connected to personal financial gain will we see change in the lifestyle habits of Americans.

The “8 Word Healthcare Solution” works in all environments; fully insured, self funded, non-insured, government programs and medical sharing organizations. Only by empowering the consumer and shifting the control back to the individual who is the true payer and receiver of all benefits, will we ever see a substantial reduction in cost.

Consumers, Government Officials, Insurance, Risk Sharing Companies and Providers all need to come together to solve the root problems of our healthcare crisis:

ACTION #1- Federal government passes legislation requiring all health insurance plans that are sold on state and federal exchanges, receive federal tax credits, qualifiy for federal tax deductions personally or corporately all need to integrate the three components of the “8 word Solution” into such plans.